I have R3 000 000 invested in SA earning 8% per annum. I am afraid that with the country’s financial problems, the rand may weaken over the next five to 10 years. Will it be advisable to rather invest in a dollar or pound sterling investment in a bank overseas and safeguard the value of my money (in rand terms)?

Without knowing the role that this money plays in your overall financial plan, I will address the considerations around the points that you have raised.

Concerns around South Africa

A common discussion that we have with clients is around the concerns of keeping your wealth invested in South Africa, be it through investment property, a local business or the local stock market. There is a very real concern that our fiscal and monetary policy may deteriorate along with the likes of our state-owned enterprises and other government-led initiatives.

Without getting into any lengthy discussions on this topic, it’s worth noting that you have the discretion to invest your money around the world in a variety of underlying global currencies. Investors who are concerned about the woes that South Africa faces may prefer to have their money invested offshore. The decision to invest offshore is unlikely to disadvantage an investor over the long term provided that the money is invested responsibly – all else being equal.

A South African resident doesn’t need to be reliant on the local economy or stock market in order to get good returns on investments.

We are fortunate that we are able to invest offshore with fairly accommodative exchange control policies. Regulation 28-compliant funds (funds that you can invest in through a retirement vehicle such as a retirement annuity) are less accommodative.

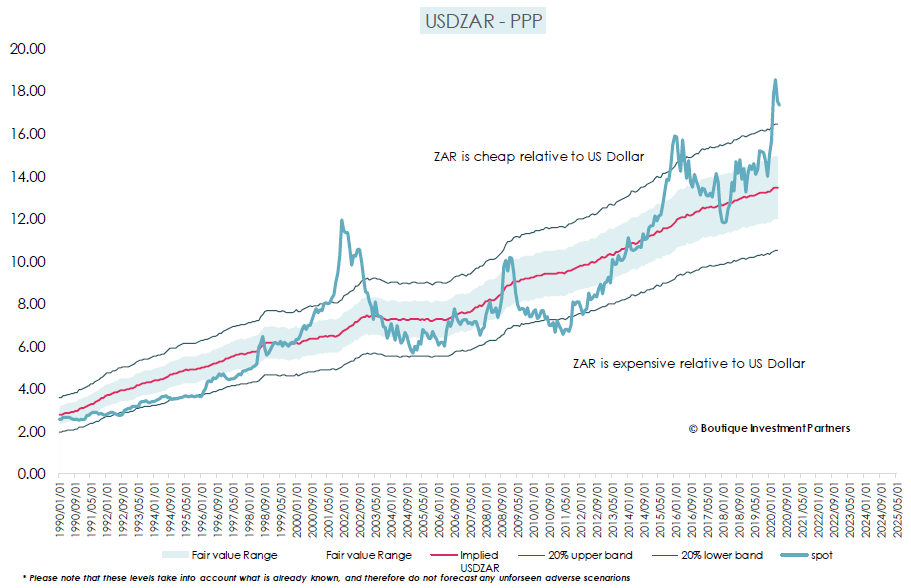

The devaluing currency

It is widely suggested that the rand is a depreciating currency over the long term. There are various fundamental reasons as to why this is believed to be the case.

However, there have been periods of rand strength over the last 30 years as shown by the graph below. Based on the purchasing power parity (PPP) of the rand-dollar exchange rate, which is a measure that is used to highlight extreme valuation signals, the rand appears to be oversold at the moment. This may suggest that there could be a rand-strengthening bias in the short to medium term. An investor with a long-term perspective is likely to continue to see the rand devaluating against major currencies such as the dollar.

Source: Boutique Investment Partners

Foreign currency investment in a bank (assumed to be cash or fixed deposit)

Based on my interpretation of your question, you are considering investing in cash or a fixed deposit instrument which is denominated in a foreign currency. There are three main considerations for this decision.

1. Inflation

Inflation globally is fairly benign, with some debate as to whether we are in an inflationary or deflationary environment with unprecedented global monetary and fiscal stimulus. The widely accepted inflationary outlook is for inflation to remain low over the short term. Cash investments are likely to devalue in the base currency over the next five to 10 years as a result of inflation (ignores rand depreciation).

2. Interest rates

Interest rates globally are at relatively extreme lows. Cash in the bank is likely to yield a negative real return and is therefore unattractive over the medium to long term.

3. Costs

Cash in the bank or fixed deposits may attract fees which could be a detractor in the performance of the investment over time.

It all adds up

Foreign cash in the bank is likely to face a headwind against inflation, low-interest rates and potential costs. One may therefore assume that it could be a poor investment despite being a potential hedge against South African centric risk factors and which might manifest as a depreciating currency.

Safeguarding the value of your money offshore

Investing offshore can be an effective way to hedge one’s wealth away from South African centric risk factors including a long-term devaluing currency. Due to structural reasons, conservative offshore investments may find it challenging to give investors real returns net of costs, inflation and tax.

Depending on an investor’s objectives, time frames, risk profile and overall financial circumstances, they may need to consider appropriate exposure to growth assets in their offshore investment which will allow their capital to grow in real terms, net of costs, inflation and tax. There are many good options in this regard, and a good financial advisor will be able to advise you appropriately.